Three investors. Same information. Same market. One panic-sells. The other doubles down. A third quietly ignores everything and keeps their money in a fixed deposit. The difference isn't intelligence, research access, or market knowledge. It's investor behaviour — and the Bailard, Biehl, and Kaiser (BBK) framework maps it precisely.

IN THIS GUIDE:

01. The two dimensions that determine your investing personality

02. The five investor types — mapped and explained

03. The BBK framework in India — how it plays out

04. Why behavioural profiling matters more than market timing

05. How advisors use the BBK framework

06. The self-assessment — which investor are you?

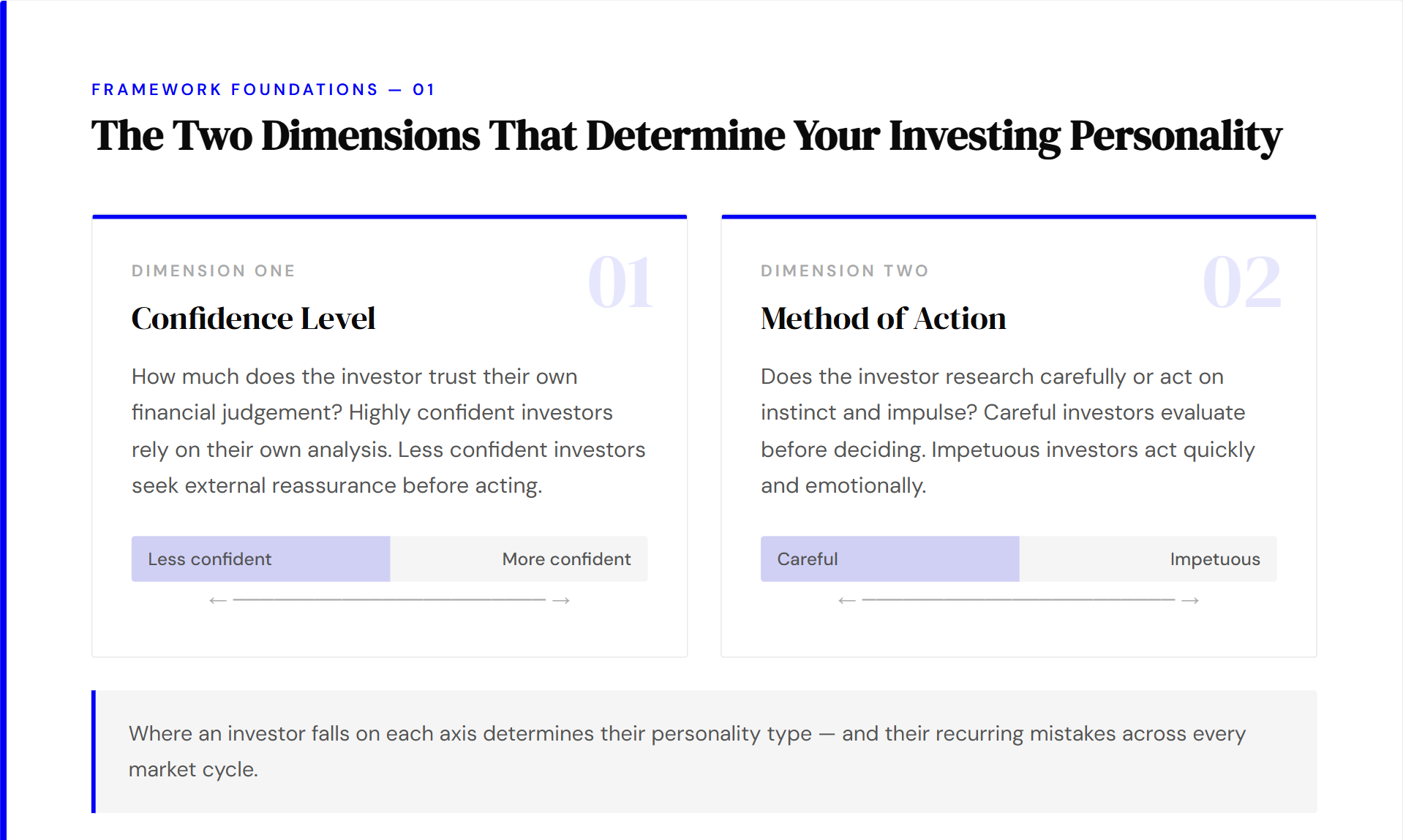

01. The two dimensions that determine your investing personality

The BBK model was developed by three American financial researchers — Bailard, Biehl, and Kaiser — who observed that investment decisions are shaped far more by psychological tendencies than by information quality. They identified two axes along which every investor naturally falls.

These two dimensions create a grid. Plot any investor on it and a distinct personality emerges — along with predictable strengths, blind spots, and investment mistakes they are likely to repeat across market cycles.

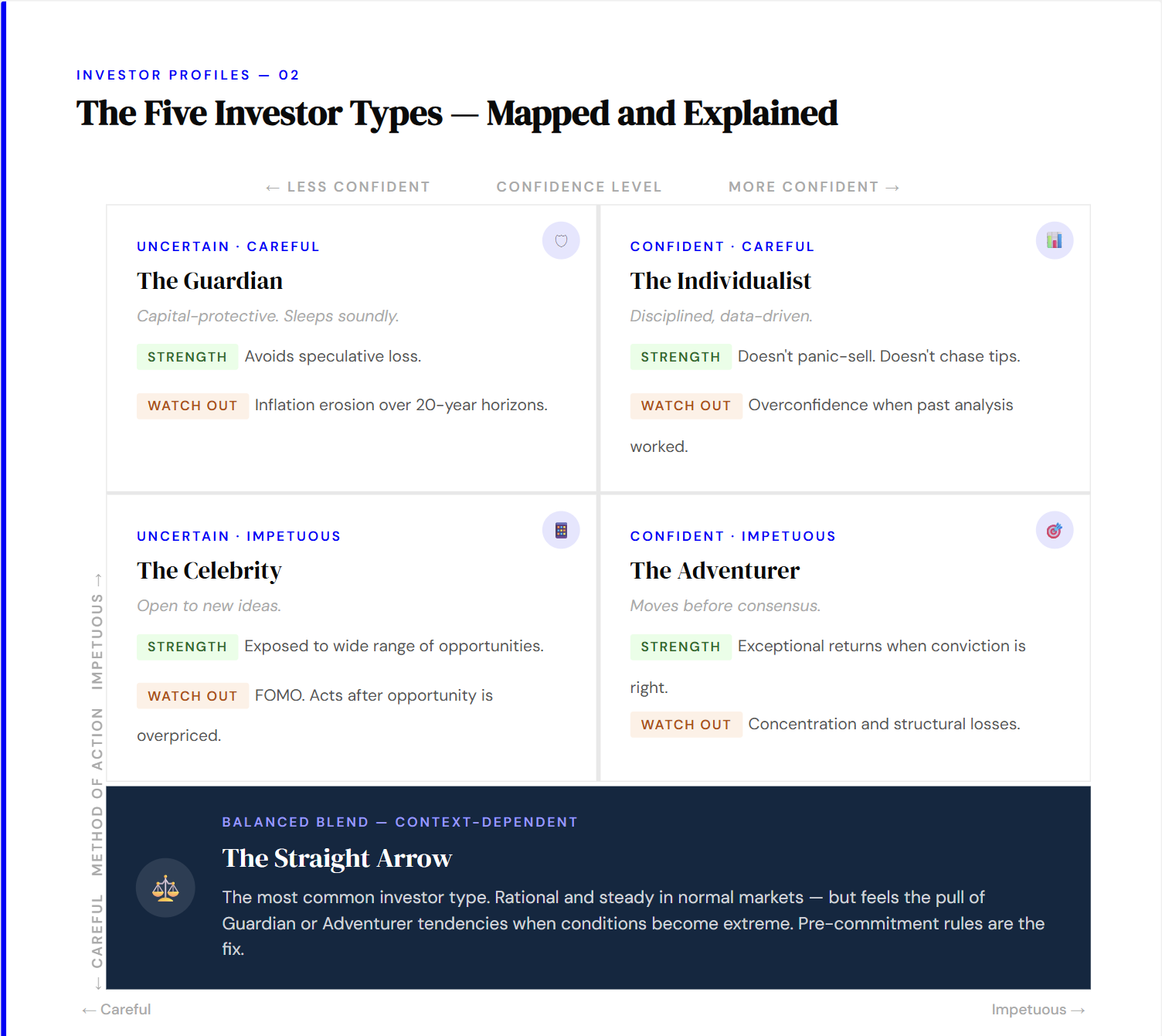

02. The five investor types — mapped and explained

The two dimensions above combine to produce five distinct investor personalities. Understanding which type you are — and which type you become under pressure —is more predictive of your long-term investment outcomes than your asset allocation.

The Individualist — disciplined but sometimes overconfident

The Individualist is highly confident and methodical. They research extensively, build diversified portfolios, and make decisions based on data rather than sentiment. During market corrections, they rebalance. During bull runs, they don't chase. Their risk is subtle: the more their own analysis has worked in the past, the more they trust it — and the harder it becomes to update when evidence contradicts it.

The Adventurer — high upside, higher exposure

The Adventurer combines high confidence with impulsive decision-making. They are drawn to concentrated positions, high-risk themes, and asymmetric bets — penny stocks, options, crypto, thematic funds at peak narrative. When right, the returns are exceptional. When wrong, the losses are structural. In India, this type is increasingly visible in social media as options-trading success stories, with the survival bias of thousands who lost quietly left out of the narrative.

The Celebrity — the FOMO archetype

The Celebrity lacks confidence in their own judgement and compensates by following external validation: WhatsApp forwards, finfluencer recommendations, telegram stock groups, trending IPOs. By the time consensus forms around an idea, the opportunity is usually overpriced. The barrier to acting on a hot tip has fallen to zero. The barrier to doing the underlying analysis has not changed.

The Guardian — preservation before growth

Guardians prioritise not losing over gaining. They keep wealth in fixed deposits, gold, real estate, and savings products. They exit equities during corrections —precisely when holding or adding would be most valuable. The emotional return from avoiding uncertainty is real and worth respecting; but over 20-yearhorizons, the cost in purchasing power erosion is substantial.

The Straight Arrow — the most common type

Most investors are Straight Arrows. They sit in the middle of both dimensions and move depending on circumstances. Calm in stable markets, they feel the pull of Guardian or Adventurer tendencies when conditions become extreme. They are context-dependent — which makes them the most responsive to structure and pre-commitment rules established in advance.

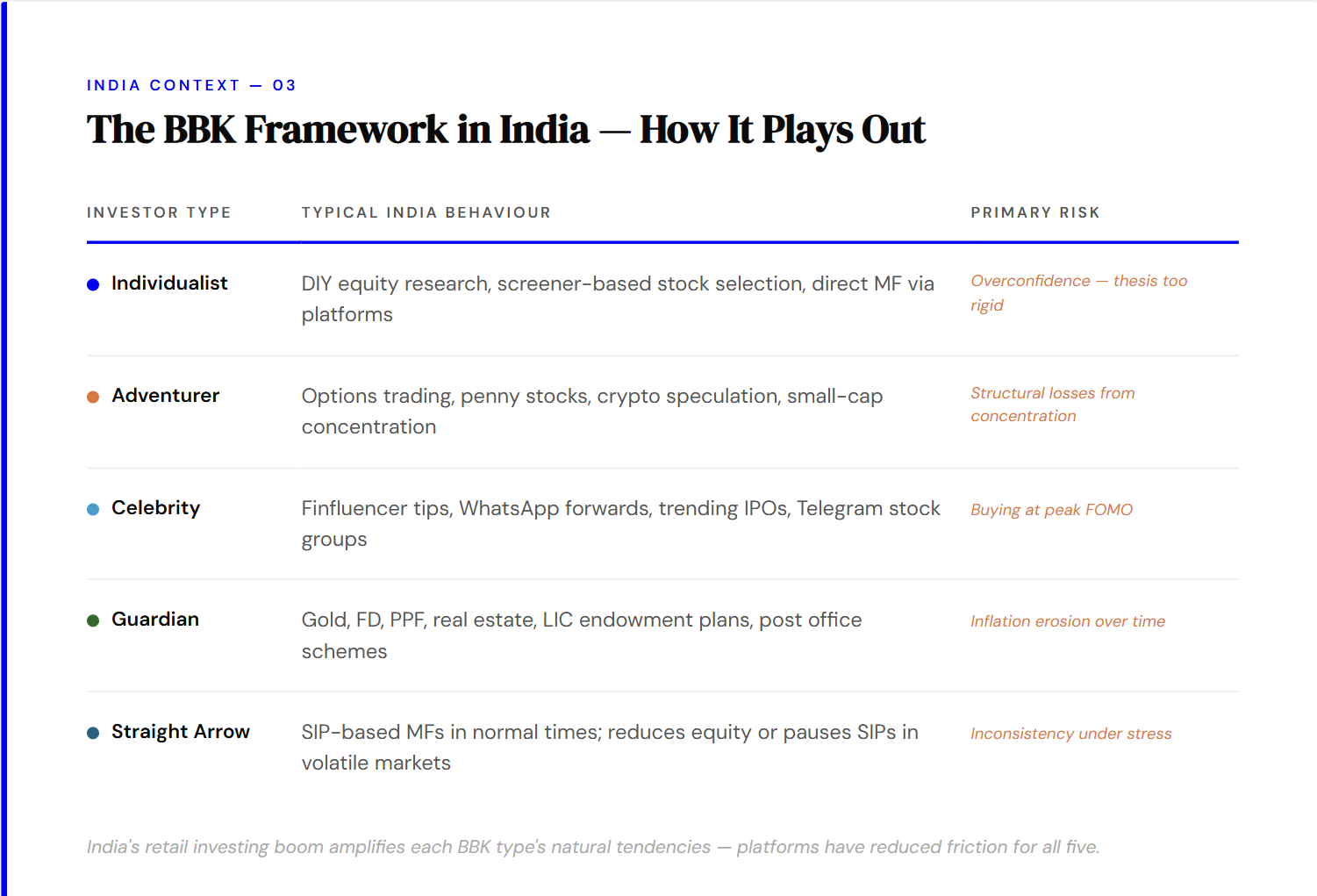

03. The BBK framework in India — how it plays out

India's unique investment landscape makes each BBK type more recognisable — and their biases more consequential. High retail participation, social-media-driven tips, a deep FD culture, and the rapid democratisation of trading platforms have amplified every type's natural tendency.

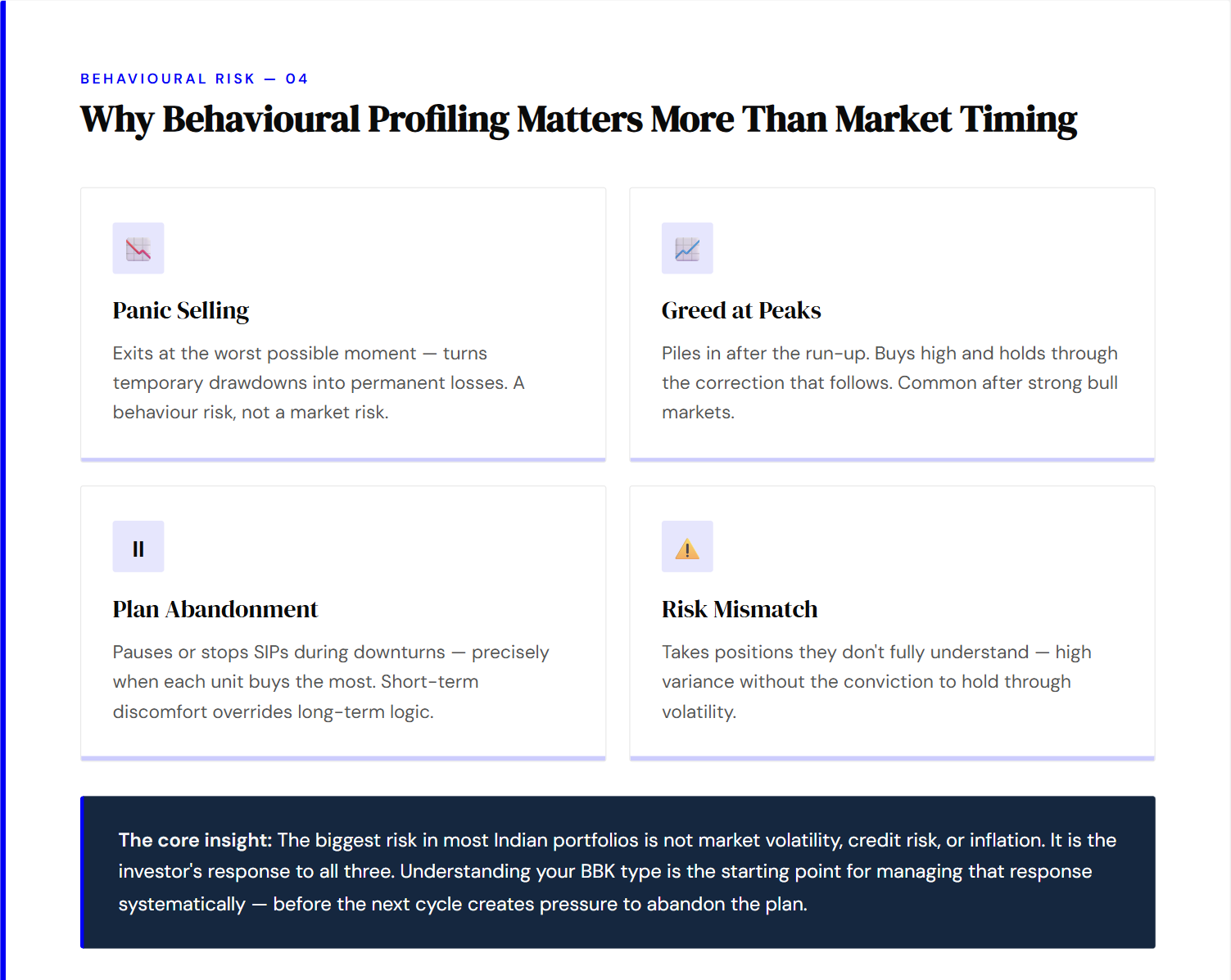

04. Why behavioural profiling matters more than market timing

Most investment failures are not caused by poor product selection. The products are largely fine. The failure point is almost always the investor's behaviour around the products — panic-selling in March 2020, overloading on crypto in2021, withdrawing SIPs when the market fell in 2022, piling into small-caps in 2024 at peak valuations.

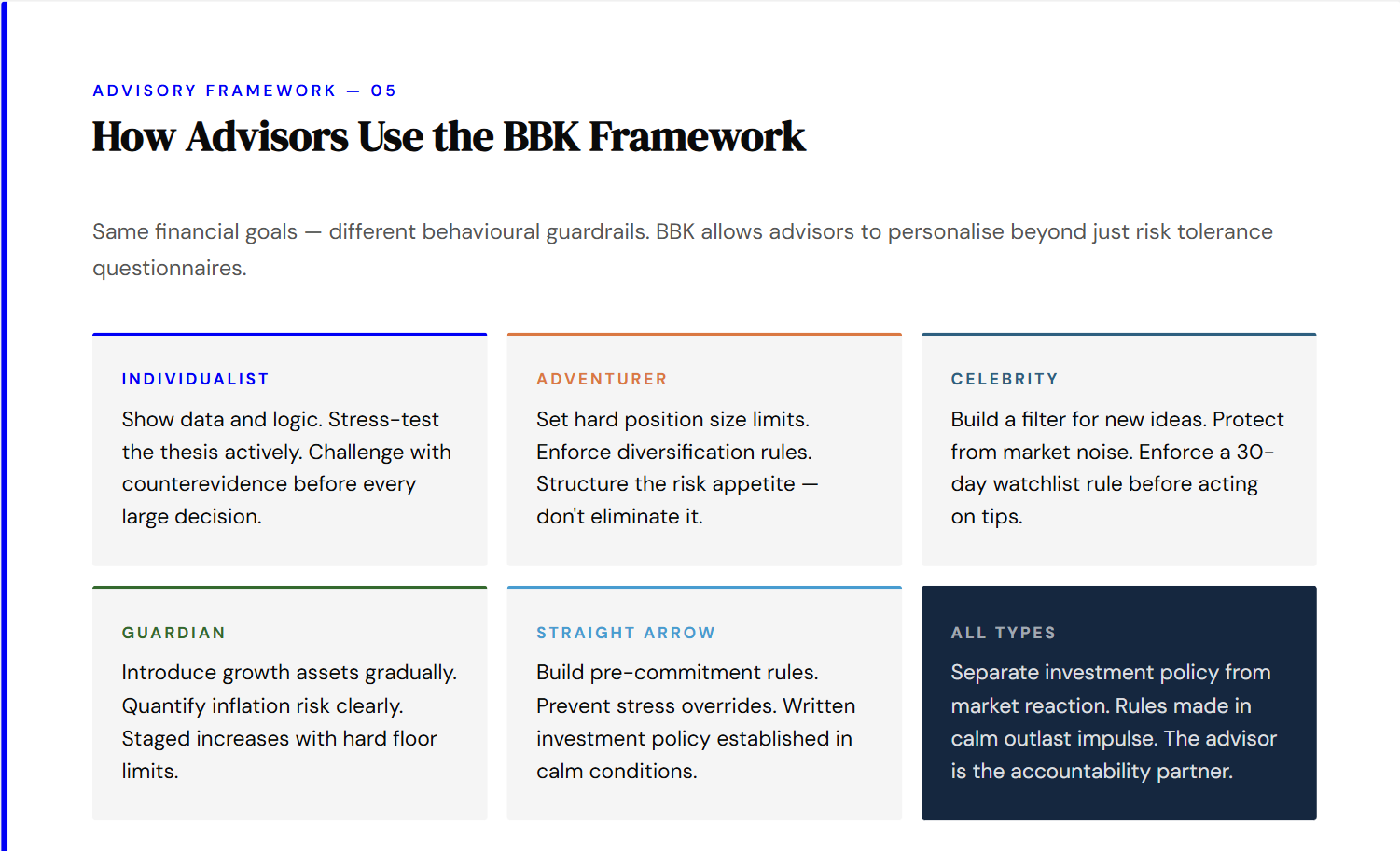

05. How advisors use the BBK framework

A good financial advisor is not just a product recommender — they are a behavioural coach. The same equity fund held appropriately by an Individualist will be panic-sold by a Guardian and traded in and out of by a Celebrity. The fund is the same. The outcome depends entirely on who owns it and what guardrails are in place.

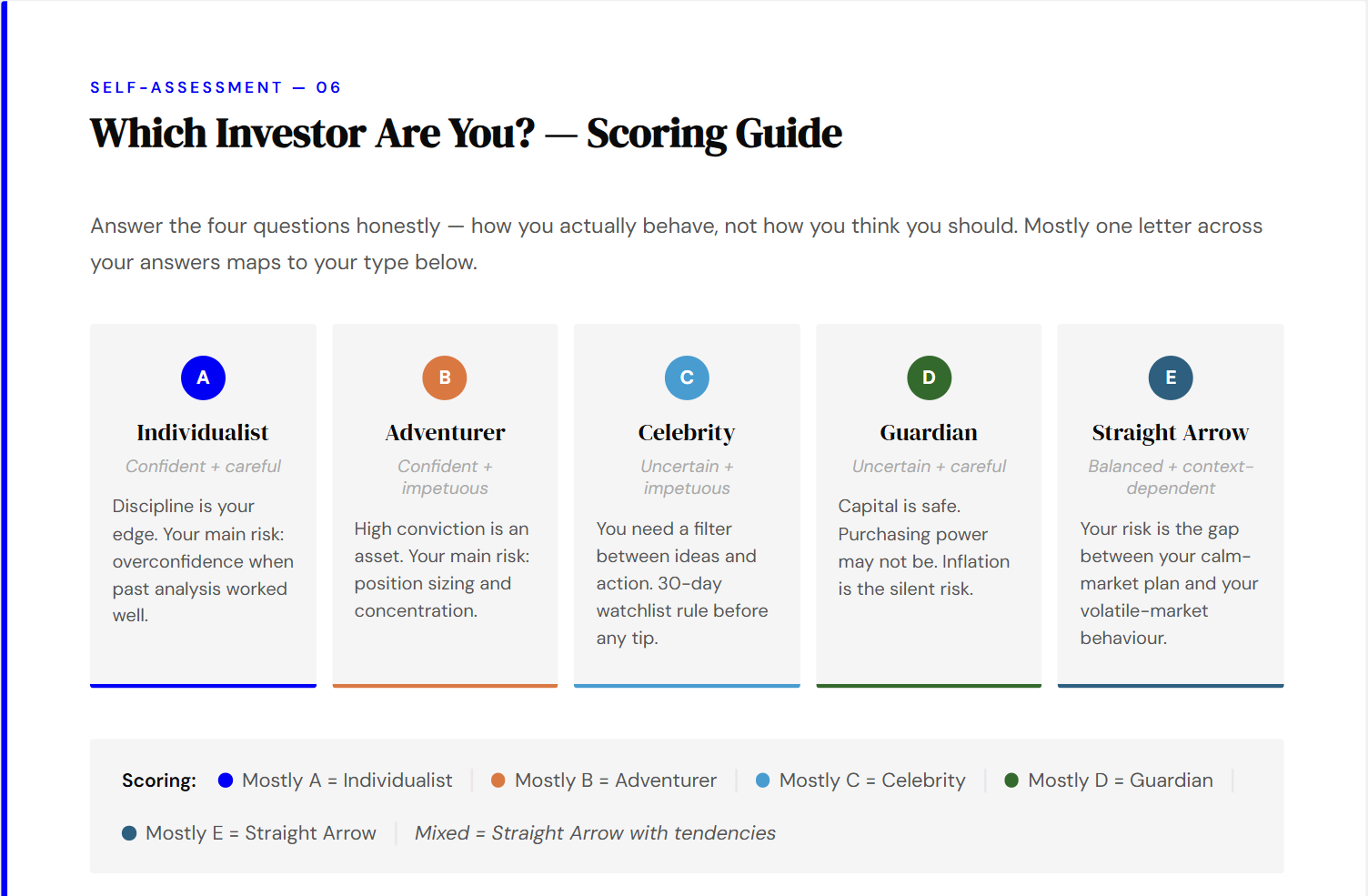

06. The self-assessment — which investor are you?

Answer the four questions below — be honest about how you actually behave, not how you think you should behave. For each question, circle or note the answer that most closely matches your genuine first reaction.

Q1. The Nifty falls 15% in a month. What do you do?

(A) Recheck my thesis. If nothing has changed fundamentally, I hold or add.

(B) Buy more aggressively — corrections are where money is made.

(C) Wait and see what experts and commentators are saying before deciding.

(D) Move at least some money out. This volatility is not worth it.

(E) Keep my SIPs going but feel uneasy and check my portfolio every day.

Q2. A friend mentions a stock that has tripled in six months. First reaction?

(A) Ask for the financials. I'll research it independently before considering it.

(B) Put a small position in today — I don't want to miss the next leg up.

(C) Lookup what others online are saying about it and consider joining.

(D) Ignore it. If it's this well-known, the risk is probably high now.

(E) Feel tempted but don't act immediately. Keep it on a watchlist.

Q3. How do you feel about having 40% of your portfolio in equities?

(A) Fine —as long as I've done the analysis to support that allocation.

(B) Too conservative. I'd prefer significantly higher equity exposure.

(C) Depends on what my advisor or what I'm currently reading suggests.

(D) A little high. I'd prefer more in fixed deposits or gold.

(E) Comfortable in normal times. I'd want to reduce if markets got rocky.

Q4. What matters most to you in any investment decision?

(A) Data quality and the soundness of the reasoning behind the investment.

(B) Upside potential. I'd rather risk losing some to gain significantly more.

(C) What experienced or popular voices are recommending right now.

(D) Capital safety. I'd rather earn less and be certain it'll be there.

(E) A balanced picture — growth, but not at the cost of sleepless nights.

Written by:

Revanth Sudish

Arpit Nagda

For suggestions/ feedback, please write to us at: research@dexterr.one

Disclaimer:

This information is for educational purposes only and should not be considered as an investment recommendation. We strongly suggest that you conduct your own research or consult with a qualified financial advisor before making any investment decisions.

Weekly newsletter

No spam. Just the latest releases and tips, interesting articles, and exclusive interviews in your inbox every week.

Thank you! Your submission has been received!

Oops! Something went wrong while submitting the form.