SIFs: The sophisticated investment structure most wealth creators haven't considered yet

SEBI has quietly introduced one of the most significant product innovations in India's mutual fund history. Specialised Investment Funds — SIFs — bring hedge-fund-style strategies into the regulated, tax-efficient mutual fund framework. If you're a seasoned wealth creator with an existing portfolio, here is what you need to understand before the market catches up with the opportunity.

IN THIS GUIDE

01. What are SIFs — and why they're different from anything in mutual funds

02. Why SEBI created them now

03. The three categories of SIFs decoded

04. Who should consider SIFs — and who should not

05. How SIFs are taxed

06. The core-satellite framework — where SIFs belong

07. Questions to ask before investing in any SIF

08. In summary

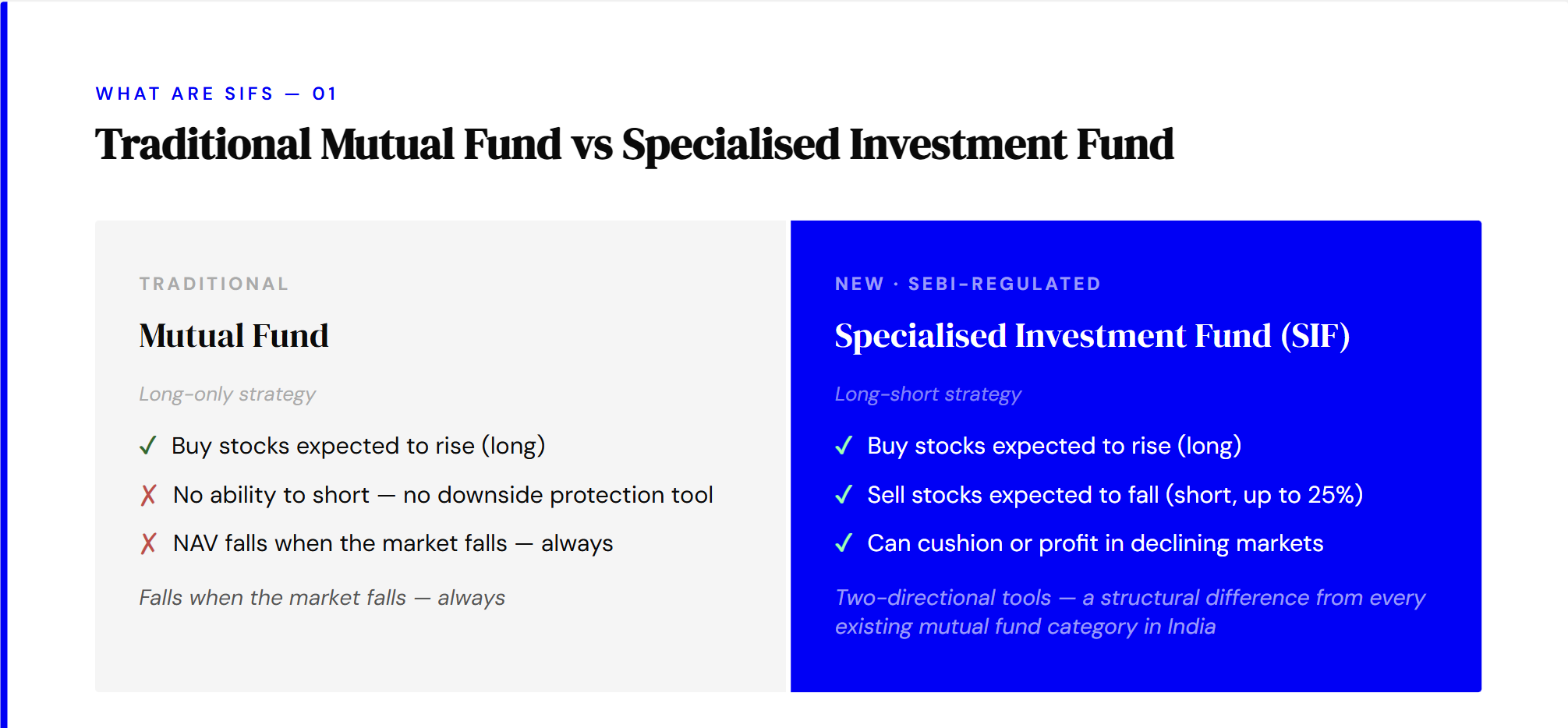

01. What are SIFs — and why they're different

Think of SIFs as SEBI's attempt to bring sophisticated investment strategies — the kind typically found in hedge funds and Category III AIFs — into the regulated, tax-efficient structure of a mutual fund. The difference from a traditional mutual fund is structural, not cosmetic.

A traditional equity mutual fund can only go long. When markets fall, your NAV falls with them. That's just the nature of directional exposure. A SIF gives the fund manager an additional tool: the ability to take short positions — to bet that certain stocks or sectors will fall — which creates the potential to generate positive returns even in declining markets, or at minimum, to cushion the downside more meaningfully than a long-only fund can.

Short exposure is capped at 25% of the portfolio for most SIF categories — this is not a free-for-all. The manager still runs a predominantly long portfolio, but the short sleeve provides a meaningful risk management and alpha-generation tool that simply did not exist in the mutual fund framework before SIFs were introduced.

02. Why SEBI created them now

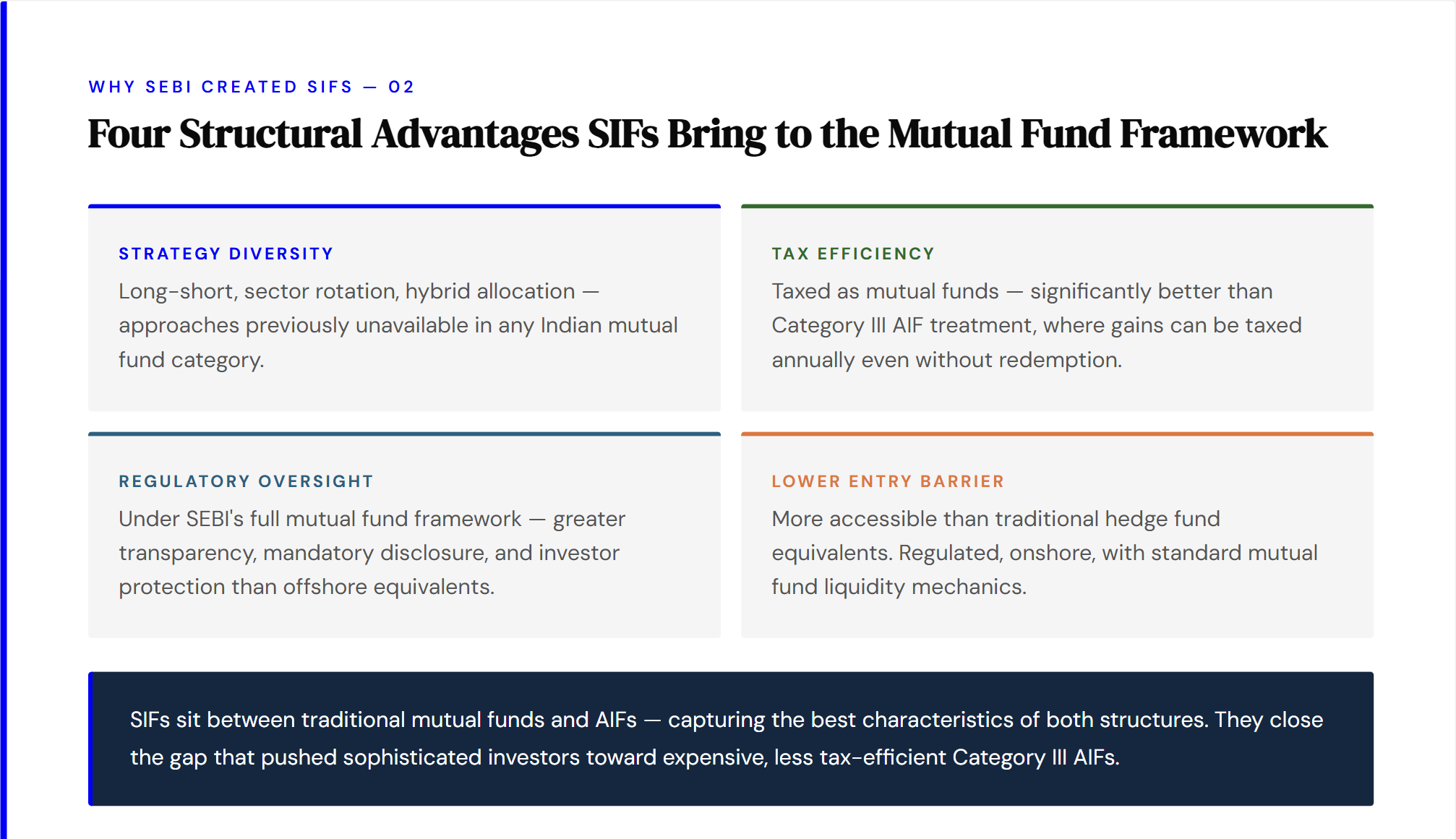

India's mutual fund industry has grown to approximately ₹76 lakh crore in AUM with over6 crore unique investors. That growth is remarkable. But for sophisticated investors managing serious wealth, the product landscape has remained relatively standardised — large-cap, mid-cap, flexi-cap, debt funds — all long-only, all subject to the same directional market exposure.

Wealthy investors who wanted actively managed downside protection or absolute return strategies were pushed toward Category III AIFs. These work, but they carry higher costs, less favourable tax treatment, and lower regulatory transparency than mutual funds. SIFs close that gap. They offer four structural advantages that didn't previously exist in a single regulated product:

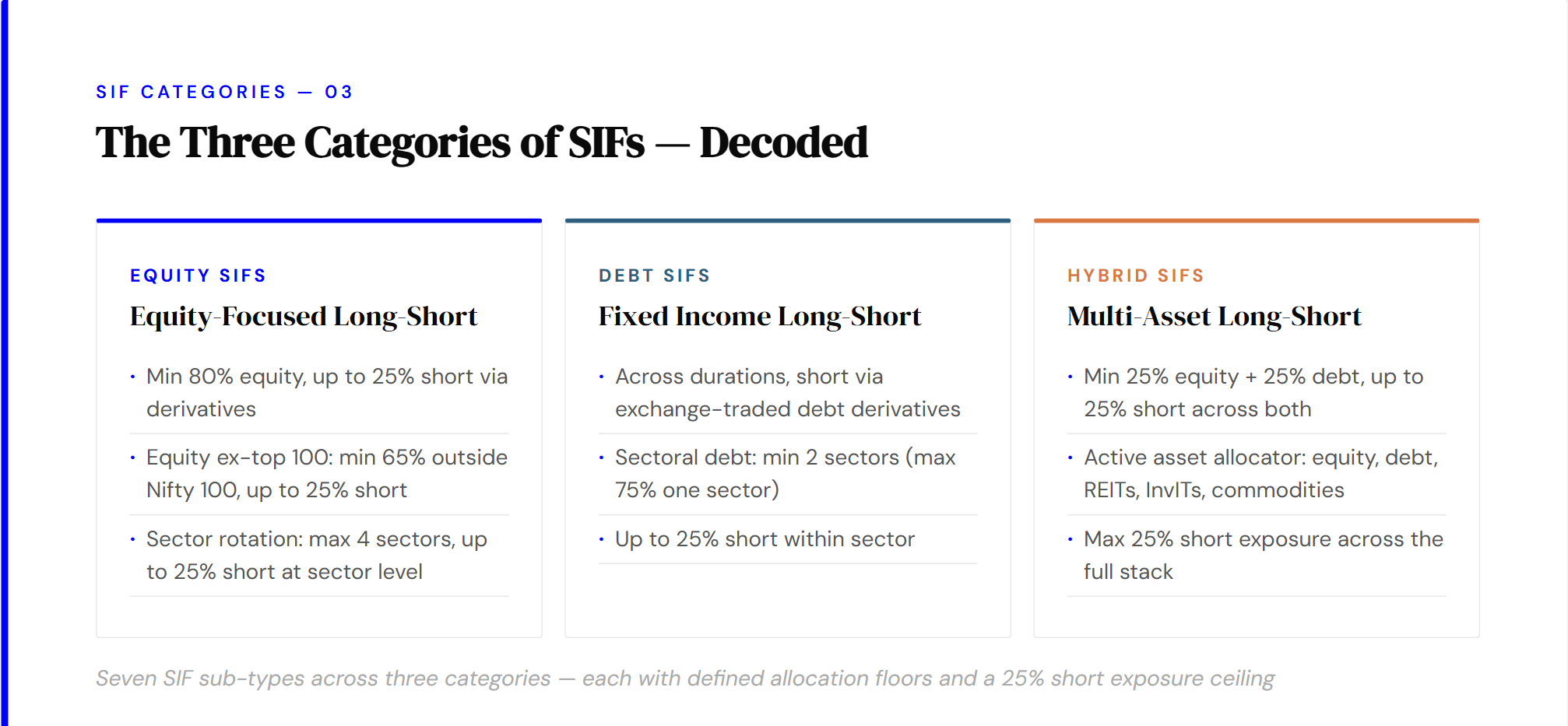

03. The three categories of SIFs — decoded

SEBI has structured SIFs into three broad categories. Each targets different objectives and risk profiles. Understanding which type suits which need is the starting point for any allocation decision — and also the point where most marketing material stops being useful.

Equity SIFs — for those who want equity exposure with a downside tool

The equity long-short SIF is the most versatile. At least 80% in equities, with the manager free to take short positions up to 25% using unhedged equity derivatives. The equity ex-top 100 variant targets mid and small-cap alpha —higher risk, higher potential reward. Sector rotation SIFs concentrate in up to four sectors and can short at the sector level — a stronger, more conviction-based bet.

Debt SIFs — for interest rate positioning

Fixed income SIFs allow duration-based and credit-relative positioning with exchange-traded debt derivative short exposure. These are not for investors seeking simple fixed returns. They are for sophisticated conservative investors who want diversified fixed income exposure combined with tactical long-short positioning — and who understand what that means in practice.

Hybrid SIFs — for multi-asset flexibility

The active asset allocator SIF is arguably the most interesting structure in the entire SIF universe. It can invest across equities, debt, REITs, InvITs, and commodity derivatives — with short exposure across the stack. For the right investor, this is one-stop access to actively managed, diversified alpha generation in a regulated mutual fund wrapper.

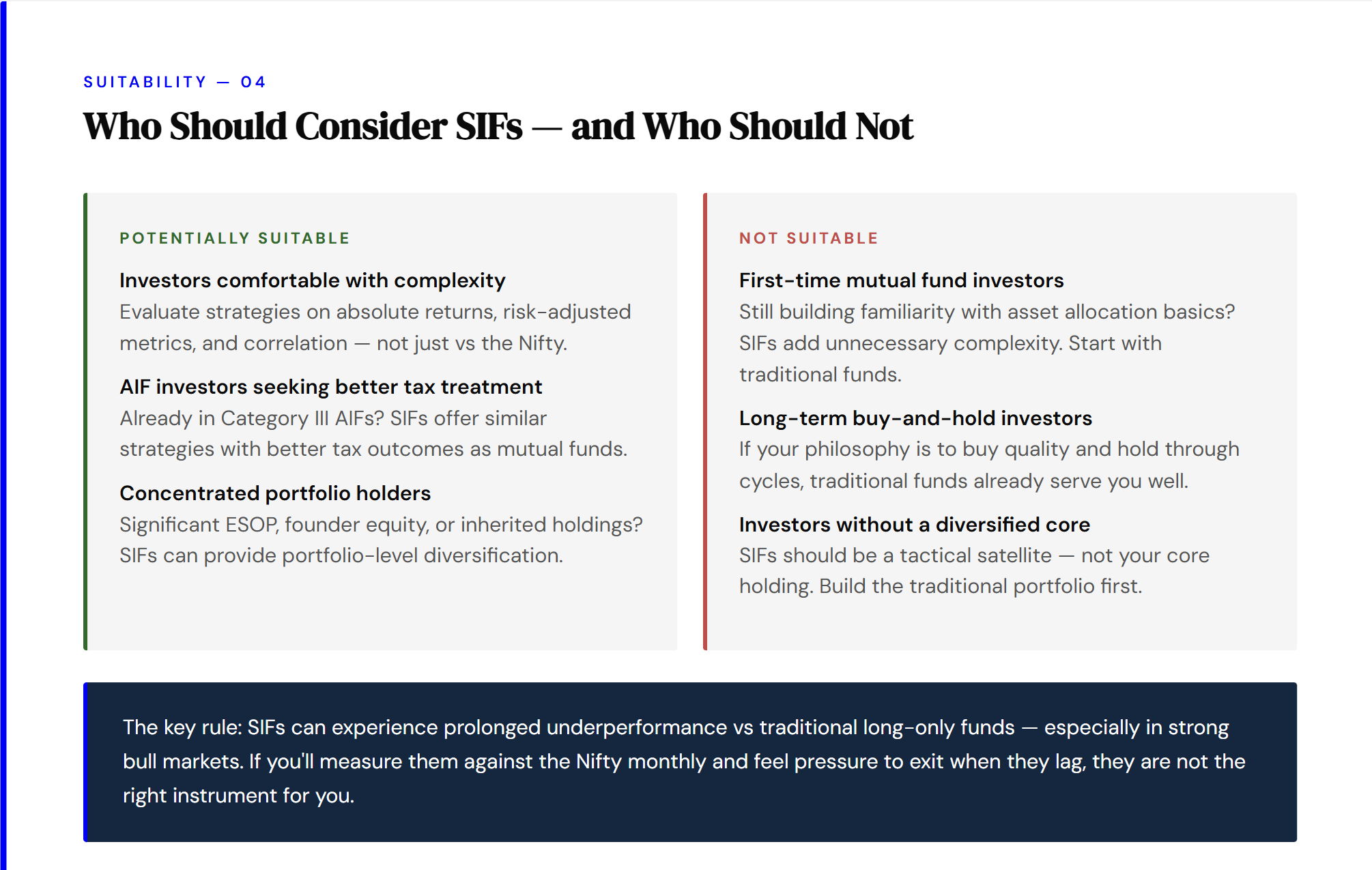

04. Who should consider SIFs — and who should not

SEBI has explicitly designed SIFs for sophisticated investors. By design, they are not appropriate for everyone — and being honest about the suitability question is as important as understanding the product itself.

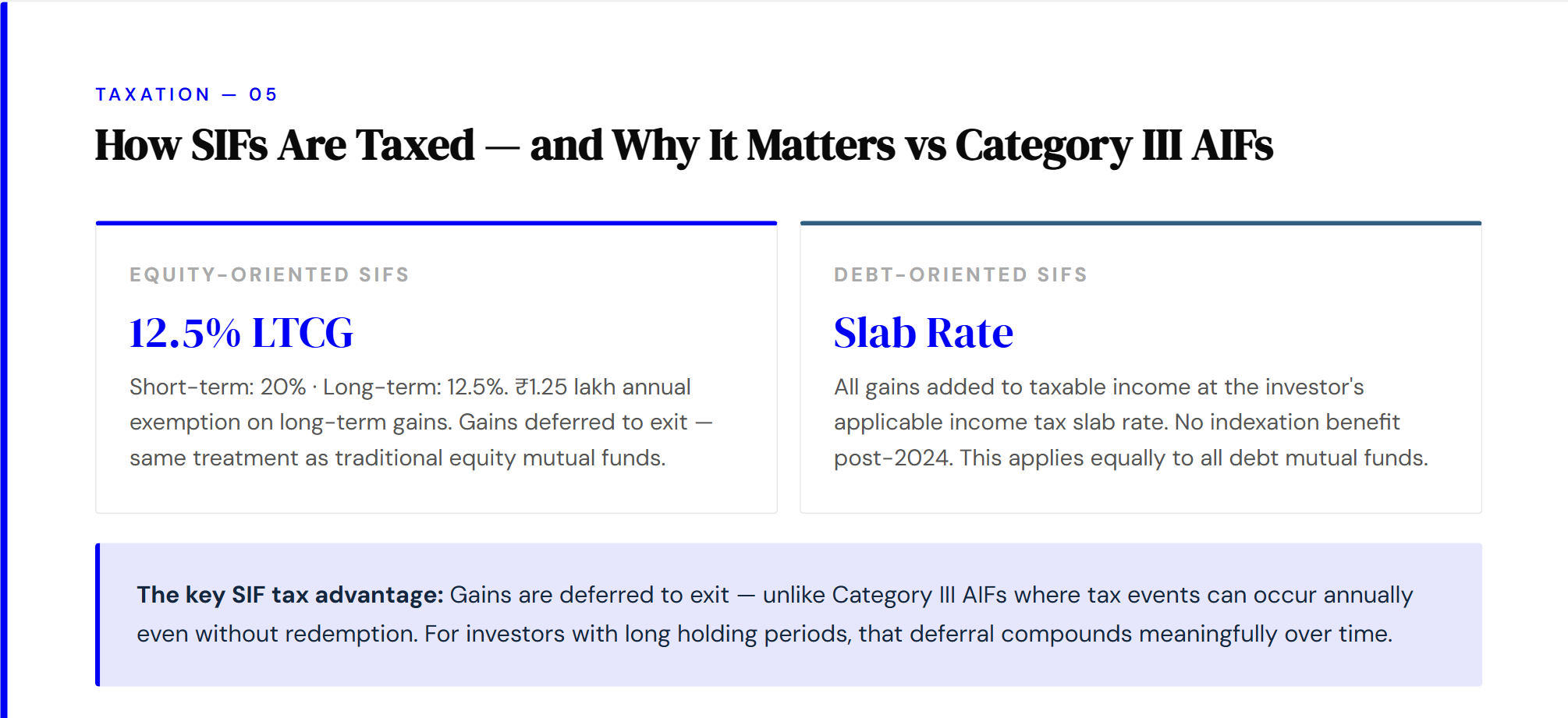

05. How SIFs are taxed

This is where SIFs have a clear structural advantage over Category III AIFs — and it's often the deciding factor for investors who are otherwise on the fence.

SIFs are taxed as mutual funds, not as pass-through vehicles that push tax liability to investors in the year it's incurred. In a Category III AIF, the fund's profits flow through to you as taxable income in the year they are realised —even if you haven't redeemed a single unit. In a SIF, you pay tax only when you exit. For investors with long holding periods, that deferral compounds meaningfully over time.

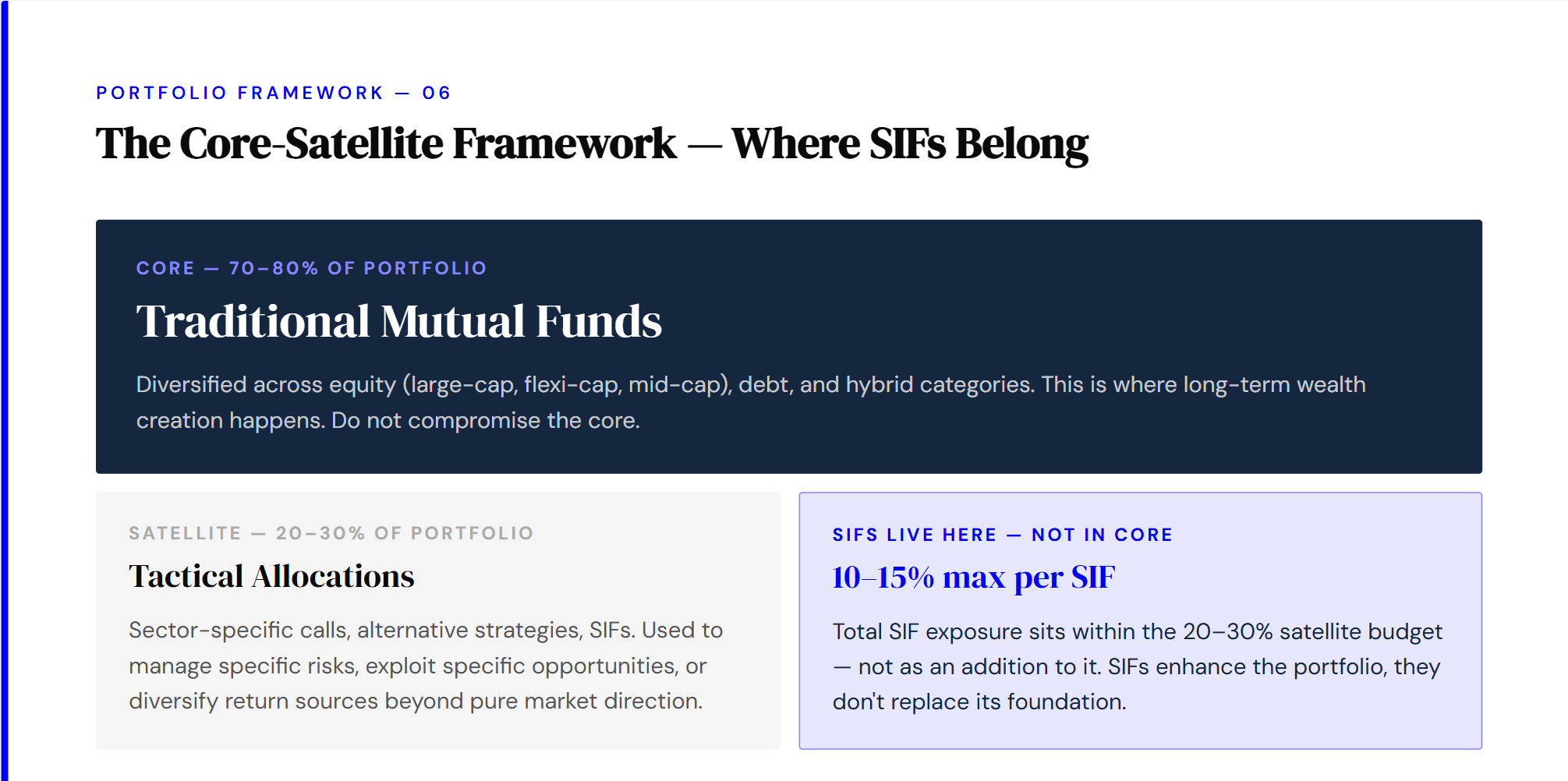

06. The core-satellite framework — where SIFs belong

SIFs are not a replacement for traditional equity or debt funds. They are a complement — with return profiles that behave differently across market conditions. The correct portfolio construction framework is core-satellite, and this distinction matters in practice.

The satellite sleeve is where SIFs can genuinely add value — managing specific risks, exploiting identified opportunities, or diversifying return sources away from pure market direction. What they should never become is a replacement for the core or the dominant equity exposure in a portfolio.

07. Questions to ask before investing in any SIF

The quality of the questions you ask before investing matters as much as the product itself. If your advisor cannot answer these clearly, that is a signal to pause — not a reason to proceed anyway.

What specific strategy does this SIF follow — and when does it underperform?

Every strategy has a market environment where it struggles. A long-short equity SIF may lag badly in a strong bull market where even weak stocks rise. A sector rotation SIF can be wrong about sector calls. Understanding the conditions under which a strategy underperforms is as important as understanding its upside — probably more so.

Does the fund manager have demonstrable long-short experience?

Managing short positions is a fundamentally different skill from managing a long-only portfolio. Many excellent long-only managers have limited or no experience running short books at scale. Ask specifically for track record in long-short or hedged strategies — not just overall fund performance. The two are not the same thing.

What percentage of my portfolio should this represent?

The answer is almost always: less than you think, and only after your core traditional portfolio is fully diversified. SIFs are satellite allocations. Most portfolios should not have more than 10–15% in any single SIF, and total SIF exposure should sit within the broader 20–30% satellite budget.

What is the total cost — including borrowing costs for short positions?

SIFs will typically carry higher expense ratios than traditional equity funds because of the complexity of running short books — margin requirements, derivative premium costs, borrowing costs for short selling. Understand the total cost of ownership before comparing net returns to a benchmark.

What is the liquidity structure —can I exit when I need to?

SIFs structured as open-ended mutual funds offer daily liquidity in principle — but the fund manager's ability to unwind short positions quickly in a volatile market may affect NAV on exit. Understand the exit provisions and any lock-in periods before committing capital.

08. In summary

Specialised Investment Funds represent the most significant structural innovation in India's mutual fund landscape since the introduction of hybrid funds. They bring strategies previously available only through offshore hedge funds or expensive AIFs into a regulated, tax-efficient mutual fund wrapper — under SEBI's full oversight.

For the right investor — experienced, well-diversified across traditional strategies, comfortable with complexity — SIFs offer legitimate tools to manage risk and diversify return sources. For everyone else, the existing mutual fund universe remains more than sufficient.

The question to ask yourself is not 'should I be in SIFs' but 'do I understand what I'm getting into, and does my portfolio actually need this right now?' If the honest answer to both is yes, SIFs are worth exploring carefully with a qualified advisor.

Written by:

Revanth Sudish

Arpit Nagda

For suggestions/ feedback, please write to us at: research@dexterr.one

Disclaimer:

This information is for educational purposes only and should not be considered as an investment recommendation. We strongly suggest that you conduct your own research or consult with a qualified financial advisor before making any investment decisions.

Weekly newsletter

No spam. Just the latest releases and tips, interesting articles, and exclusive interviews in your inbox every week.

Thank you! Your submission has been received!

Oops! Something went wrong while submitting the form.