Active Funds Underperformance – Temporary phenomenon or the beginning of an endless streak?

The debate of Active v/s Passive investing has been an endless one. Traditionally, it was largely dominated by the American context but as the Indian Markets mature, Indian Investors have joined the bandwagon too. And for all the right reasons.

The debate of Active v/s Passive investing has been an endless one. Traditionally, it was largely dominated by the American context but as the Indian Markets mature, Indian Investors have joined the bandwagon too. And for all the right reasons.

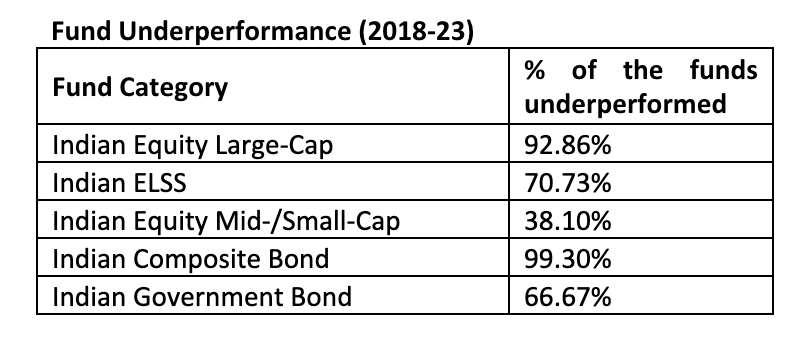

As per SPIVA (S&P Index vs Active) India Mid-Year Report 2023, a staggering 92.9% of the Active Large Cap Funds underperformed the Index over a 5-year Holding Period.

While the above table represents a very appealing argument against Active Investing, the 2 key questions one should ask are:

Why did a large number of Large Cap Funds Underperform the Index?

The Funds that did manage to beat the Index, what’s the secret of Performance?

Answering these 2 simple questions can help us understand if these trends will hold in the future as well or if these are just one-offs.

Let’s take 1st Question. In the year 2018, SEBI noted that AMCs (Asset Management Companies) had become a tad too creative with the nomenclature and structure of Mutual Fund schemes. Increasingly, AMCs were resorting to Scheme names that appeared more enticing and offered zero understanding of the Fund Itself. Case In Point: “Income Opportunities Funds” which invested in the bonds issued by relatively low-rated companies thereby exposing investors to the Credit Risk (Risk of Default).

SEBI realised that Mutual Funds Ecosystem needed standardization. It did 2 things: 1. Clearly defined all the Categories in which Mutual Funds could be created thereby creating 16 Categories across Equity & Debt Funds. 2nd, it mandated that names should reflect the Category in which the Mutual Fund Scheme falls thereby making it easy for people to understand the nature of the fund they are investing in. Overnight, the Income Opportunities Funds were renamed to Credit Risk Funds.

As an Extension of Point 1, what SEBI also addressed the Structure of these Funds. SEBI Defined each category with good detail. For example, Large Cap Funds will now have to have 80% of their Portfolio (by AUM) allocated to top 100 companies of the country. This meant, restricting the Fund Manager’s universe in the large part of the fund. Active Fund Managers in the past had up to 30-40% exposure to Mid and Small Cap space. More often than not, it is the Mid & Small Cap exposure that led to the Alpha (Over Performance) generation. For more details on each category, you can refer to this link: https://www.amfiindia.com/investor-corner/knowledge-center/SEBI-categorization-of-mutual-fund-schemes.html

So, with the wings of liberty clipped, will the Large Cap Fund Managers still be able to beat the index? Well, theoretically, Yes. Practically, anybody’s guess. The data for the last 5 years surely suggests otherwise.

This brings us to our 2nd question: What’s the secret “Alpha Sauce” that helped the small number of Fund Managers create the Over-Performance? Can this Alpha Sauce be consistently reproduced?

To answer this question, it’s important to understand that Fund Managers and their Analyst/ research teams are constantly working towards developing and testing their Investment Models. They are constantly reinventing these models, evaluating newer ideas, and striving to beat not just index returns but every other fund manager. But, nothing guarantees Alpha. At least, the data suggests so. An ET Money Study of the Performance of the top 92 Mutual Fund Schemes between 2013 to 2023 found that:

Not even a Single Scheme was consistently in top Quartile across these 10 Years.

Only 4 Schemes could be in first Quartile 80% of the times.

Some of the Funds had extreme swings. Case in Point: Axis Bluechip Fund. From being a top Quartile Fund in 2020 it dropped to last Quartile the immediate next year.

All this evidence points toward the fact while Fund Managers do have their recipes for Alpha Creation, they surely have zero control over the Actual Alpha Creation. Their Alpha Sauce works some years, some years it just doesn’t.

Another interesting observation has been around Active Funds Shutting down. As per SPIVA report 2023, roughly 30% of the funds in the large cap space have closed down in the last 10 years. Which 1 trigger of this could be SEBI’s recategorization of MF Schemes, the events of Active Funds closing/ merging schemes are surely not rare.

Before I conclude this piece and share my views, I think it’s also very important to understand the Quality of the Alpha created. You see if an Active Fund over-performs the Index by even as small a margin as 0.1%, it will fall in the category of Out-Performing funds. The important question hence is, how much is the overperformance aka Alpha?

Of the Funds that beat the Index, more than 60% beat it by less than 0.5% or 50 bps. This also reflected in the average category performance, which has not been able to beat the index in the last 10 years as per the SPIVA Report.

While the debate on Active vs Passive is just getting started in India, our firm belief is that increasingly, across the categories, Fund Managers would find it difficult to beat their respective Benchmarks. As Index Investing catches on, the Purchase Patterns of stocks will change. Every constituent of the Index will get rewarded to the extent of its weight thereby leaving no space for any Human Bias. Index Investing will also increase the stock research pool in India and make information more readily available on a larger number of companies. This will make Fund Managers work harder on unearthing “Hidden Opportunities”. This said, Fund Managers will surely be relevant and keep churning Alpha in certain categories.

India’s capital markets are just getting ready for a new movement if not a revolution. Passive Funds are surely the way forward for most of the Indians. The question is not whether you should invest in Passive. The right question is, how much of your Portfolio should be allocated to Passive? Watch this space, we will answer this soon. Till then, read this report here: https://www.spglobal.com/spdji/en/documents/spiva/spiva-india-scorecard-mid-year-2023.pdf .

See you soon!

Weekly newsletter

No spam. Just the latest releases and tips, interesting articles, and exclusive interviews in your inbox every week.

Thank you! Your submission has been received!

Oops! Something went wrong while submitting the form.